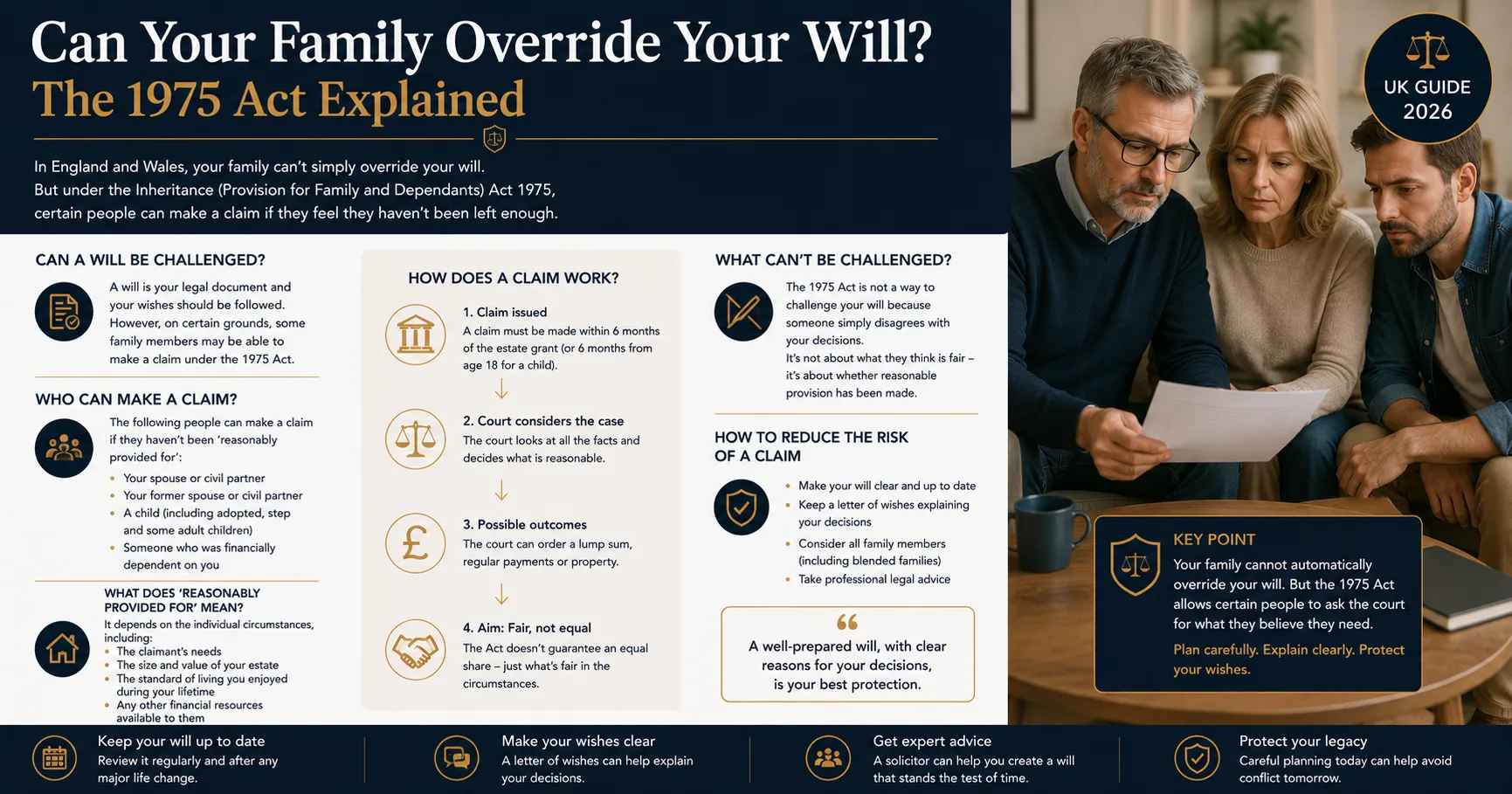

Most people assume that if you write a valid will, it's the final word. You decide who gets what; the law enforces it. That's mostly true — but not entirely. Under the Inheritance (Provision for Family and Dependants) Act 1975, certain people can apply to the court to vary your will after you die, even if your will is perfectly valid and clearly worded.

This isn't a backdoor for distant relatives or anyone who feels hard done by. The 1975 Act is narrow, specific, and time-limited. But if you're disinheriting a child, leaving a long-term partner out, or making unusual provision for a dependant, it pays to understand how the Act works — because failing to plan around it can mean your wishes are overridden by a judge.

What the 1975 Act actually does

The Inheritance (Provision for Family and Dependants) Act 1975 lets specific categories of people apply to the court for "reasonable financial provision" out of your estate when they believe your will (or the rules of intestacy) failed to provide for them.

The court has wide powers. It can order lump sums, periodical payments, transfer of specific property, settlement of property on trust, or variation of trusts already created. It cannot rewrite your will line by line — it adjusts the financial outcome to make reasonable provision for the successful applicant.

Crucially, the Act does not give a general right to challenge a will. It doesn't matter that your nephew thinks you should have left him the boat. He has to fall within one of the eligible categories and show that the will failed to make reasonable financial provision for him.

Who can apply?

Section 1 of the Act lists the categories. They are:

- The deceased's spouse or civil partner.

- A former spouse or former civil partner who has not remarried or formed a new civil partnership (and who hasn't been barred from claiming under the terms of a divorce settlement).

- A cohabitee who lived with the deceased in the same household, as if they were spouses or civil partners, for the whole of the two years immediately before the death.

- A child of the deceased — including adult children, biological or adopted.

- Anyone treated by the deceased as a child of the family in relation to a marriage, civil partnership, or where the deceased was a single person who acted as a parent (for example, stepchildren in some cases).

- Any other person who, immediately before the death, was being maintained by the deceased — wholly or partly — financially.

Notice what's missing: parents, siblings, friends, and distant relatives generally have no standing under the 1975 Act unless they were being financially maintained by you.

What does "reasonable financial provision" mean?

This is where the Act distinguishes between two standards:

- The surviving spouse standard. Spouses and civil partners are entitled to "such financial provision as it would be reasonable in all the circumstances of the case for a husband or wife to receive, whether or not that provision is required for his or her maintenance." This is roughly the standard a divorce court would apply if the marriage had ended in divorce rather than death.

- The maintenance standard. Everyone else is entitled to "such financial provision as it would be reasonable in all the circumstances of the case for the applicant to receive for his maintenance." Maintenance is broader than bare subsistence — it covers reasonable living standards — but it's not the same as a fair share of the estate.

Adult children claiming under the Act face a harder test than spouses. They need to show actual financial need, and the courts have repeatedly said that an adult child in good health and capable of working has no automatic claim on their parent's estate. But it's not impossible — disability, financial dependency, long-standing estrangement caused by the deceased, and other factors all weigh in.

If you're thinking through how to reduce the risk of a 1975 Act claim against your own estate, our guided will builder prompts you through the relevant family situations and flags areas where extra documentation is likely to help.

What the court considers

Section 3 of the Act sets out the factors a court must consider on any application:

- The financial resources and needs of the applicant — now and in the foreseeable future

- The financial resources and needs of any other applicant or beneficiary

- Any obligations and responsibilities the deceased had towards any applicant or beneficiary

- The size and nature of the estate

- Any physical or mental disability of any applicant or beneficiary

- Any other matter, including conduct, that the court considers relevant

For spouse claims, the court also considers age, length of marriage, and the contribution made to the family — domestic and financial.

Time limits — six months from grant of probate

This is critical. An application under the 1975 Act must normally be made within six months of the grant of probate or letters of administration. The court can extend the deadline in exceptional circumstances, but it's discretionary and not guaranteed.

This means executors should think carefully before distributing the estate quickly. If they distribute everything within six months and a 1975 Act claim then succeeds, they can be personally liable to make good the shortfall. The standard practice is to wait at least six months — and often longer if there are signals a claim might come.

Common situations where 1975 Act claims arise

In our experience the same patterns recur:

- Estranged adult children. A parent disinherits a child in favour of a new partner, charity, or other children. The disinherited child applies, especially if they're financially dependent or disabled.

- Cohabiting partners excluded from the will. Partners who lived together for years but never married, where the will is old or doesn't mention them. We covered this in detail in our cohabiting couples UK will guide.

- Second-marriage situations. A surviving spouse is left only a life interest, and adult children from a previous marriage feel squeezed out. Both sides can have valid claims. Blended families and wills explores the planning options here.

- Dependants who weren't relatives. A long-term carer, a disabled friend who was being maintained, an adult child of a former partner. If maintenance was being provided, the claim is on the table.

- Cases of intestacy. The 1975 Act applies equally where someone dies without a will — see dying without a will UK for how the rules of intestacy can throw up the same problems.

Want to reduce the risk of a 1975 Act claim? Trusted Hands turns these decisions into a 15-30 minute guided builder. Start free → — only pay when you download.

How to plan around the 1975 Act

You can't contract out of the 1975 Act. But you can reduce the chances of a successful claim — and the chances of one being brought at all — by being deliberate about how you structure your will:

- Don't go silent on disinheritance. If you're leaving someone out who might otherwise expect to inherit, write a contemporaneous letter of explanation. It won't prevent a claim, but courts give weight to a clearly reasoned explanation.

- Provide for dependants properly. If someone has been financially dependent on you, leaving them nothing or a token gift almost guarantees a claim. Consider a discretionary trust or maintenance provision.

- Use trust structures for second marriages. A life interest trust for the surviving spouse with capital flowing to the children of a previous marriage is a well-established approach. It needs careful drafting.

- Document gifts and lifetime support. If you've already given someone significant help during your lifetime, record it. It feeds into the "obligations and responsibilities" factor.

- Update the will after major changes. Marriage, divorce, a new partner, a new child. All of these change the cast of potential 1975 Act claimants.

For complex estates, we recommend you seek assistance from a Trusted Hands Advisor or your own legal advice — particularly where you're knowingly excluding a child or partner, or making unusual provision.

Frequently asked questions

Can my will be completely overturned by a 1975 Act claim?

No. The court doesn't void your will. It varies the financial outcome by ordering provision for the successful claimant — usually out of the residuary estate, sometimes from specific gifts. The rest of the will stands.

Does it apply if I die without a will?

Yes. The 1975 Act applies equally to estates passing under the rules of intestacy. If the intestacy rules fail to provide for an eligible dependant, they can claim the same way they could if there had been a will.

My adult son hasn't spoken to me in 20 years — can he still claim?

He can apply, but it doesn't mean he'd succeed. Courts have rejected claims by capable adult children with no financial need, particularly where the estrangement was their doing. The outcome depends heavily on the facts.

How much does a 1975 Act claim cost?

It varies enormously, but contested 1975 Act claims regularly cost tens of thousands of pounds in legal fees on each side, often more. That cost typically comes out of the estate — meaning whatever the result, the beneficiaries get less.

Can I write something into my will that prevents claims?

No. You can't contract out of the Act. You can use careful drafting, letters of explanation, and trust structures to make claims less attractive — but you can't shut the door entirely.

Ready to write your will?

Trusted Hands is a guided, plain-English will builder. You answer simple questions, see your draft as you go, and only pay when you're ready to download.

- Free to start — no card details to begin

- Smart Will Engine — only asks what's relevant to your situation

- Fixed price — no hourly bills, no surprises

- Annual updates option — keep your will editable as life changes