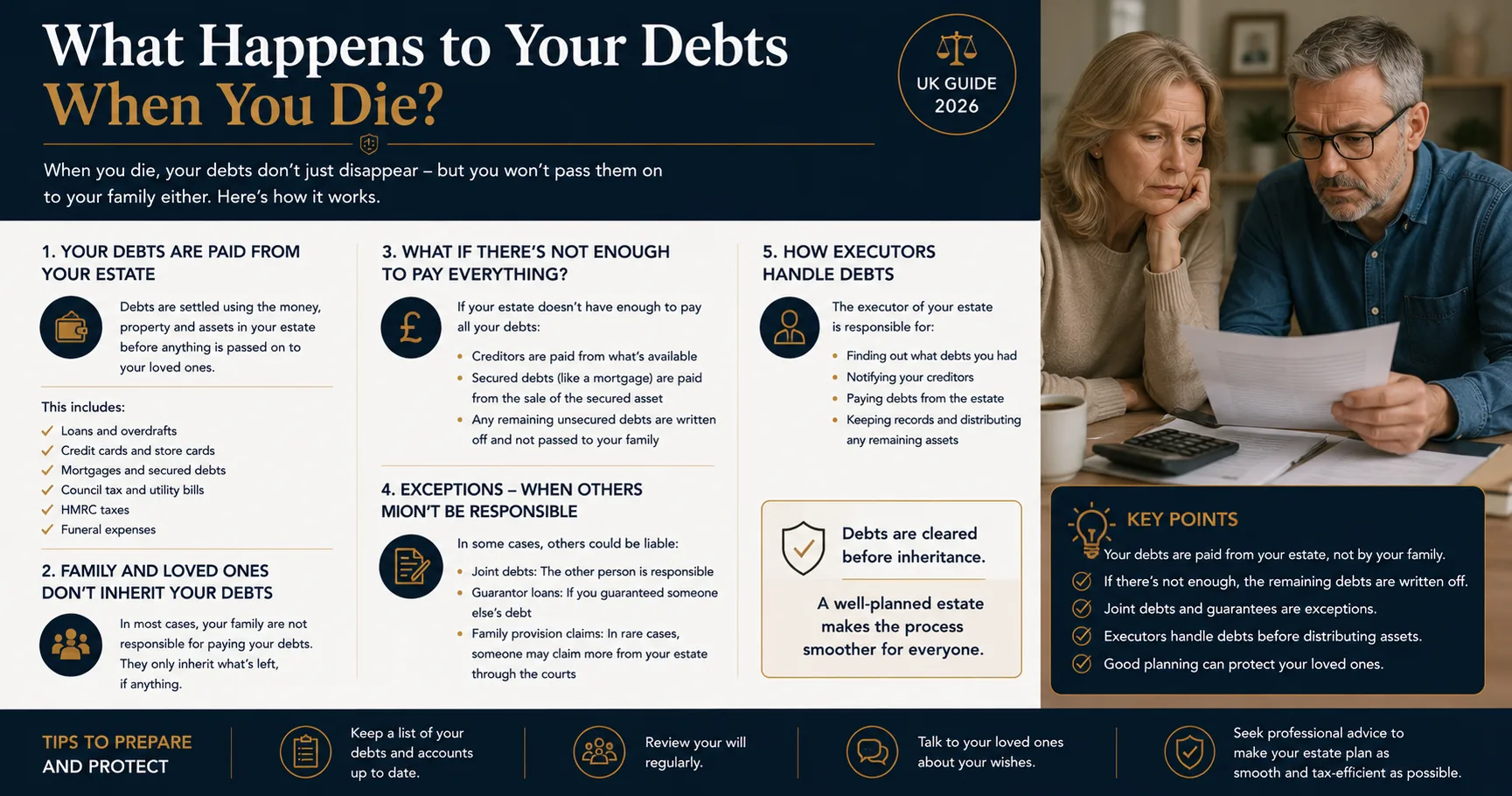

A common worry when someone dies is whether their debts pass to the family. The short answer for most UK situations is: no, debts don't pass to your relatives personally. They get paid from the estate, and if there isn't enough to go round, they often go unpaid.

The longer answer involves a few important exceptions, a fixed legal order of payment, and some real pressure on whoever is acting as executor. Here's how it works.

The basic rule: debts are paid from the estate

When someone dies, the executors (or administrators, if there's no will) are responsible for:

- Identifying all the debts

- Identifying all the assets

- Paying the debts in the right order

- Distributing whatever's left to the beneficiaries

Beneficiaries don't inherit debts — they inherit what's left after debts. So if dad dies owing £15,000 on credit cards but leaves a £200,000 estate, the credit cards get paid first; the children share whatever remains.

If the estate is insolvent — debts greater than assets — there is nothing left to pass on, and the unpaid creditors usually have to write off the balance. There is no general principle in English law that family members must "step in" to cover the difference.

When you do become liable

The exceptions are important:

- Joint debts — if you co-signed a loan, mortgage, or overdraft with the deceased, you remain fully liable for the whole amount, not just your share.

- Personal guarantees — if you guaranteed a business loan or rental, the lender can still chase you under the guarantee.

- Debts in your name — bills you ran up jointly (utilities, council tax for a property you co-occupied) remain yours.

- Mortgages on jointly-owned property — the surviving owner usually inherits the obligation along with the property.

If you've simply been named in the will, or you're next of kin, you do not become personally liable for the deceased's debts. That worry is widespread but unfounded for the most part.

We've covered the related question of what happens to bank accounts on death in a separate guide.

The legal order of payment

The Administration of Estates Act 1925 and the Insolvency Act 1986 set out the order in which debts must be paid. Executors who get this wrong can be personally liable, so it's worth knowing.

For a solvent estate (assets cover all debts), the order is broadly:

- Funeral expenses

- Testamentary expenses (probate fees, estate administration costs)

- Debts secured against assets (mortgages — usually paid by the asset itself)

- Unsecured debts (credit cards, loans, utility arrears, tax)

- Specific gifts under the will

- Residuary beneficiaries

For an insolvent estate, the priorities are tighter:

- Reasonable funeral expenses

- Testamentary expenses

- Preferential debts (some employee wages, etc.)

- Ordinary unsecured debts (paid pro rata if there isn't enough)

- Interest on the above

- Deferred debts (loans from a spouse, for example)

Executors should not pay out to beneficiaries until they're confident debts have been settled. Paying too early and discovering a debt later is the classic executor mistake.

These are exactly the kinds of pitfalls our guided will builder warns about when you're considering who to appoint.

What executors should do first

If you're an executor of an estate that may have debts, the practical sequence:

- Place a section 27 notice in The Gazette and a local paper. This invites any creditors to come forward within two months. Once that period ends, executors who paid out the estate without knowing about a debt are protected from personal liability for it.

- Write to known creditors with the death certificate and ask for final balances and any insurance that might apply.

- Don't pay anything out of order — pay funeral expenses, then secured debts via the relevant assets, then unsecured debts, then beneficiaries.

- Keep records — every executor decision should be documented. If a beneficiary or creditor challenges later, the records are the defence.

- Consider professional help for anything complex.

We've covered the broader executor role in our guide on how to choose your executors.

Specific debt types — what happens

Credit cards and personal loans: unsecured. They go into the queue with other unsecured creditors. If the estate can't pay, the balance is written off. Some accounts have payment-protection insurance that clears the balance on death — always worth checking.

Mortgages: secured against the property. The mortgage is usually settled either by life insurance or by selling the property. If the property is jointly owned, see our guide on jointly owned property for how survivorship affects this.

Council tax and utilities: continue to accrue until the property is sold or someone else takes it on. Council tax is often discounted or exempt during probate — speak to the local authority.

Tax owed to HMRC: treated as an ordinary unsecured debt for most purposes. The estate's own tax liabilities (income tax to date of death, capital gains tax on assets sold by executors, inheritance tax) are testamentary expenses paid before unsecured debts.

Student loans: UK student loans (Plan 1, 2, 4, 5, postgraduate) are written off on death. They don't pass to the estate.

Funeral expenses: can be paid out of the deceased's bank account before probate — banks will usually release funds for a reasonable funeral on production of an invoice and the death certificate.

Hire purchase / car finance: the asset can be returned to settle the debt, or the family can settle the debt and keep the asset.

Overdrafts: unsecured. If the deceased held the account jointly, the surviving holder is liable for the full amount.

Inheritance tax — paid by the estate before beneficiaries see anything

Inheritance tax is technically a debt of the estate. It's paid by the executors before distribution. The £325,000 nil-rate band and £175,000 residence nil-rate band (frozen until April 2030 under current government policy) determine how much, if any, is owed. Full details are in our inheritance tax guide, and the typical timeline runs alongside the rest of probate.

Want to leave clear instructions for your executors? Trusted Hands turns these decisions into a 15-30 minute guided builder. Start free → — only pay when you download.

What if there's not enough money to pay everyone?

An insolvent estate is one where debts exceed assets. Two practical paths:

- Informal administration — executors pay out in the legal order until funds run out and creditors lower in the queue go unpaid. The remaining debts are written off. This is by far the most common.

- Formal insolvency administration — the estate is administered under the Administration of Insolvent Estates of Deceased Persons Order 1986. Used for complex insolvencies where formal protection is needed.

Beneficiaries in an insolvent estate inherit nothing, but they inherit no debt either. For complex estates, we recommend you seek assistance from a Trusted Hands Advisor or your own legal advice.

Frequently asked questions

If my parent dies with credit card debt, do I have to pay it?

No — not unless you were a joint account holder, signed a personal guarantee, or were already a co-debtor. Your parent's estate pays from their assets. If there's nothing left, the credit card company writes the balance off. Some companies will still write to relatives asking for payment; you do not have to pay.

What about debts in joint names?

Joint debts remain fully your responsibility. The lender can pursue you for the entire balance, not just your share. This includes joint mortgages, joint loans, and joint credit cards.

Can creditors take the house?

Yes, if the house was security for a debt (a mortgage), or if it's the only significant asset and the estate's debts can't otherwise be paid. Beneficiaries don't get to keep the house if there isn't enough other money to settle the estate's debts.

How long do creditors have to claim?

If the executors place a section 27 notice in The Gazette and a local paper, creditors have two months to come forward. After that, executors who have distributed the estate are protected. Creditors may still pursue beneficiaries who received their inheritance, but executors are off the hook.

Does life insurance count as part of the estate?

Usually no — if the policy is written in trust or has named beneficiaries, the payout goes directly to them and bypasses the estate. That means it can't be claimed by creditors (and it doesn't count for inheritance tax in most cases). If the policy isn't in trust, the payout falls into the estate and is available to creditors.

Ready to write your will?

Trusted Hands is a guided, plain-English will builder. You answer simple questions, see your draft as you go, and only pay when you're ready to download.

- Free to start — no card details to begin

- Smart Will Engine — only asks what's relevant to your situation

- Fixed price — no hourly bills, no surprises

- Annual updates option — keep your will editable as life changes